Quantitative equity research

Original research at the

1-day to 30-day horizon.

The information gap between high-frequency execution and fundamental analysis. Too slow for systematic flow desks. Too fast for sell-side coverage. Underserved by institutions — and where Unfair publishes.

Notes synthesize SEC filings, insider transactions, congressional disclosures, credit spreads, options flow, dark-pool prints, and short-interest velocity into structured event-driven and breakout research. Methodology is transparent; backtests are walk-forward; analysis is single-author.

Latest research

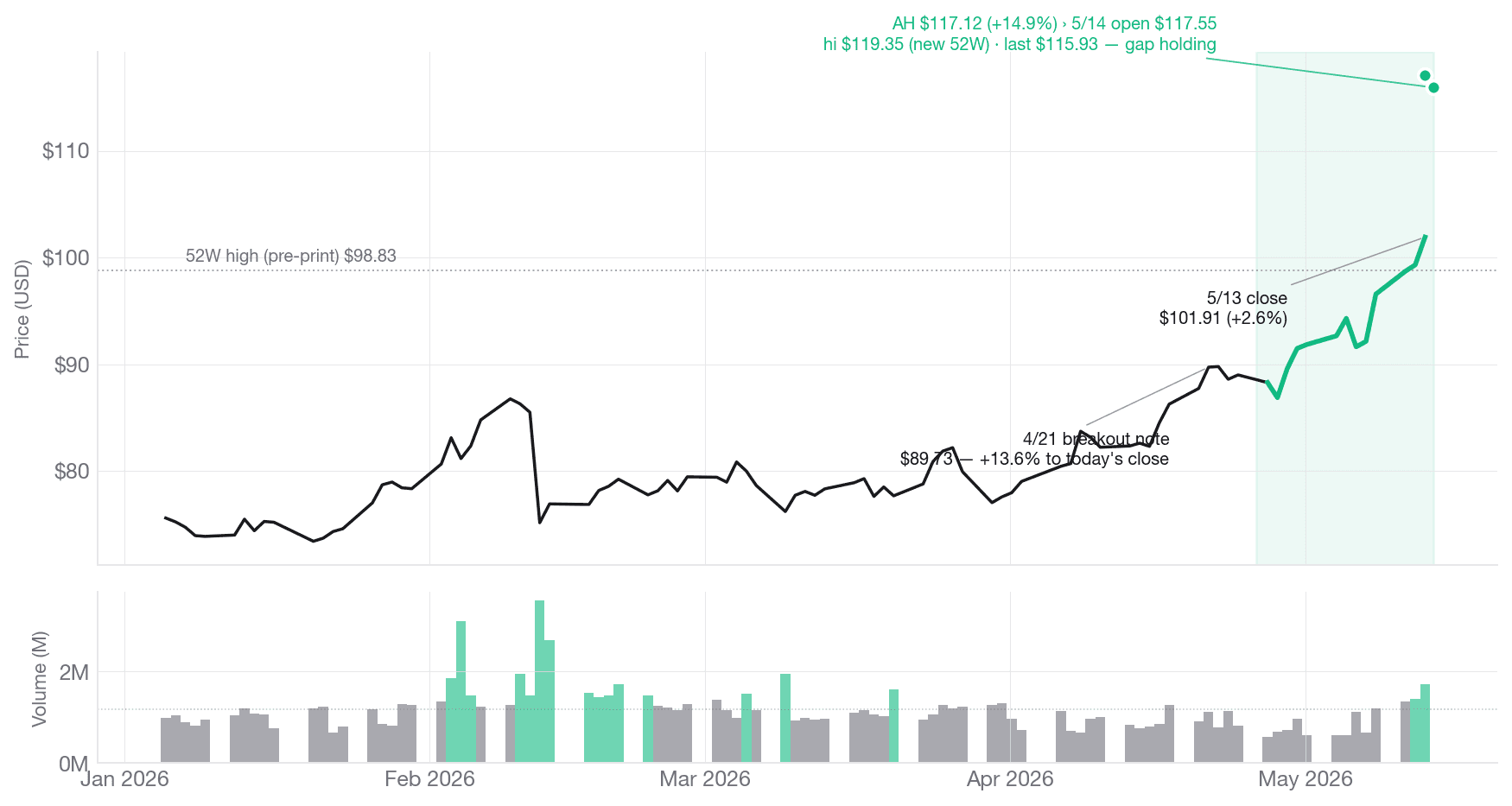

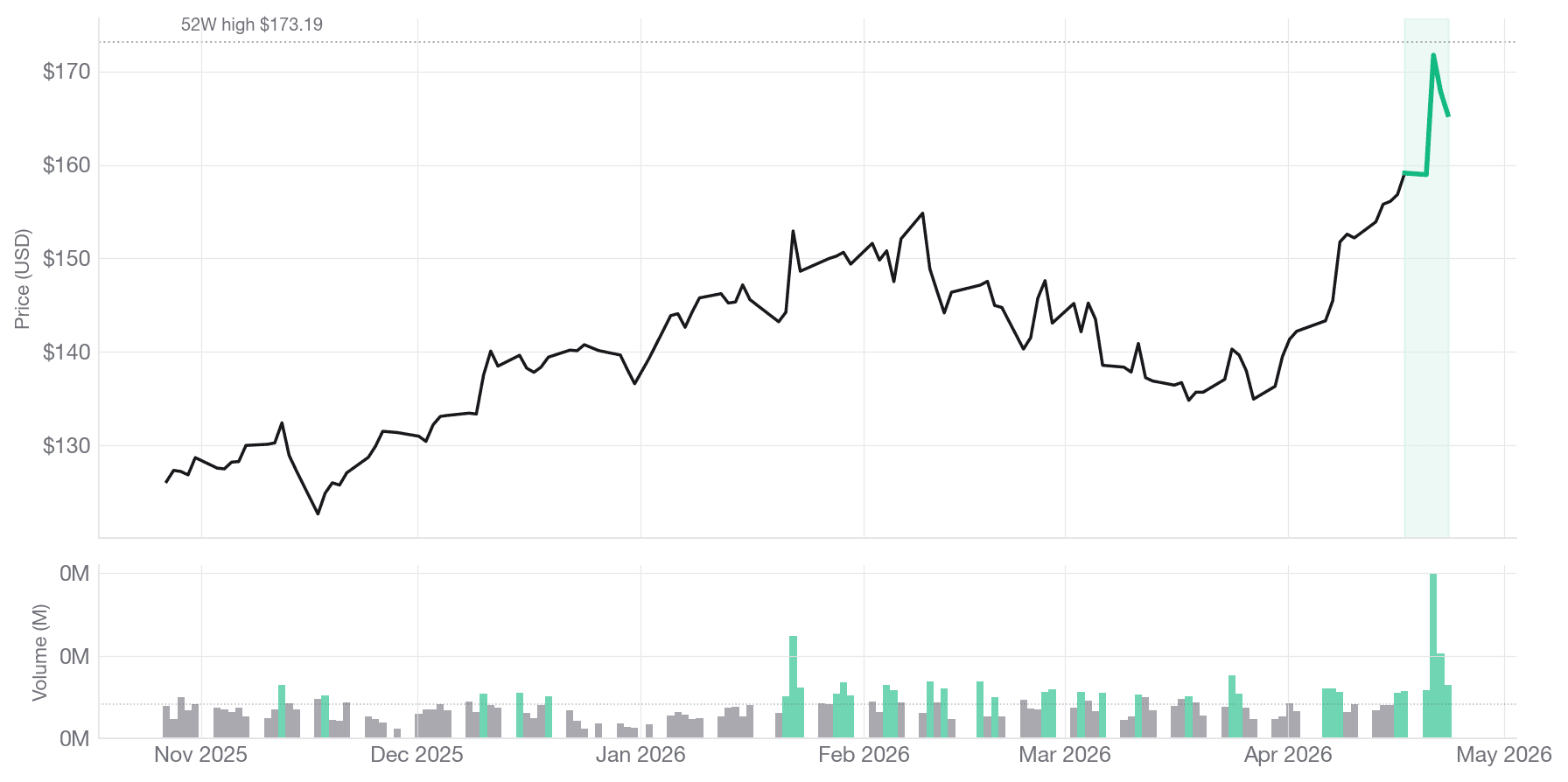

2026-05-13

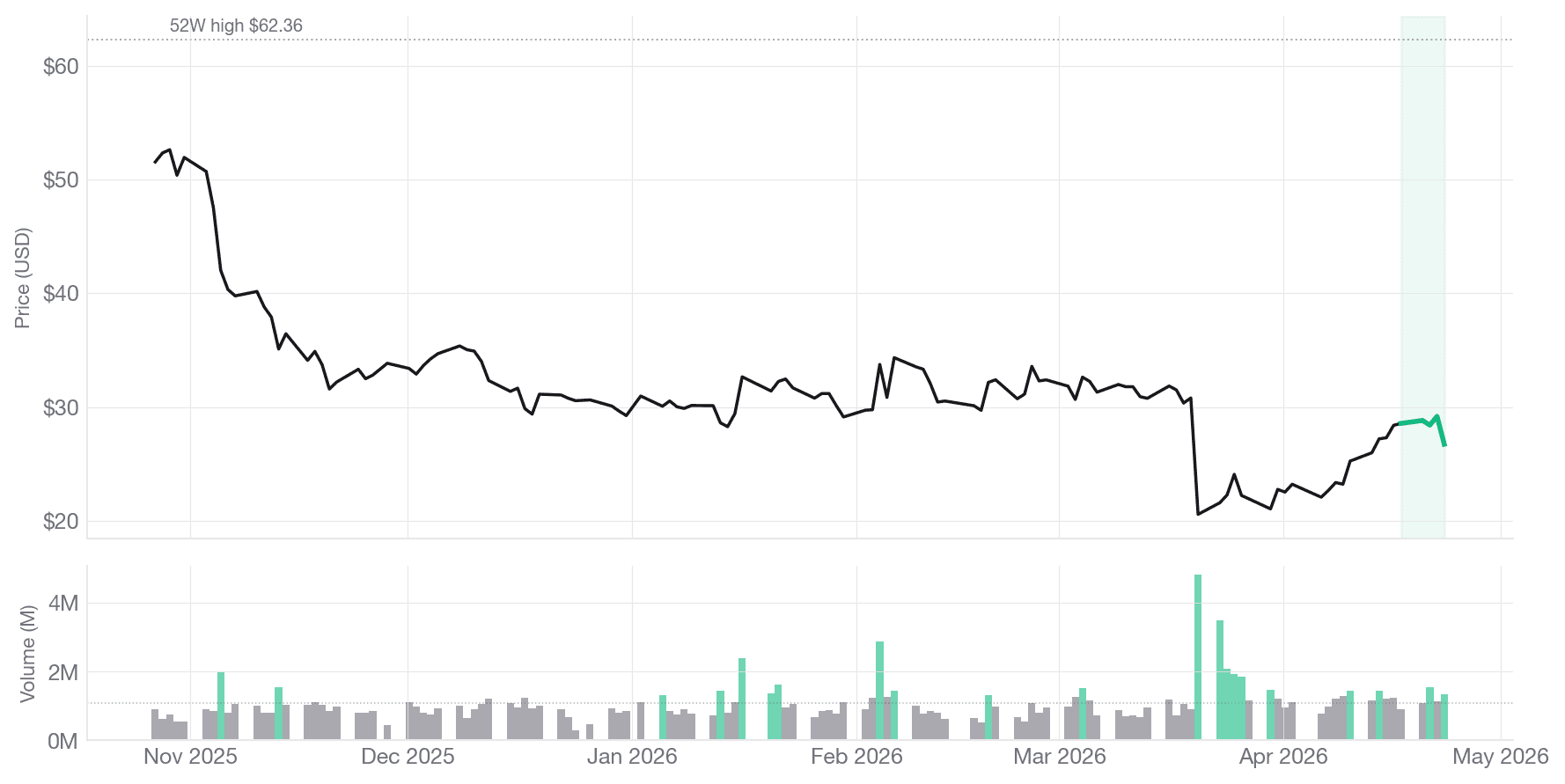

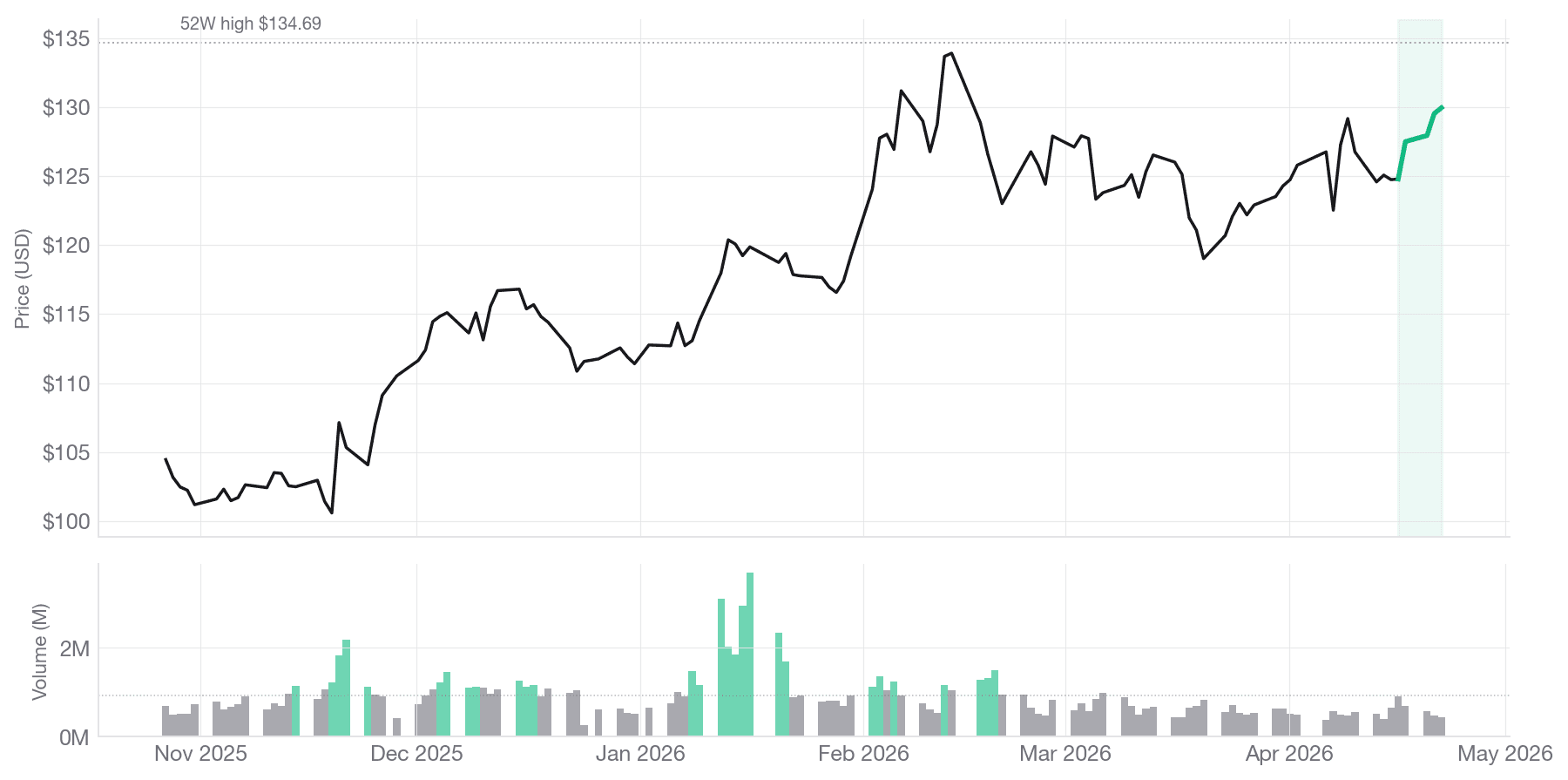

Q3 FY2026 earnings refresh — beat, raise, restructure

Record $15.8B revenue (+12% YoY), Networking +25%, AI orders FY26 raised $5B → $9B. Same-day restructuring of <5% of workforce framed as capital reallocation into silicon, optics, security, and AI. AH +14.9%. Triple-pass sentiment analysis on the unedited call transcript.

Read note →Research index

19 published notes

Options-spike signal triage

Extreme call skew with above-average premium concentration. 5-hypothesis ranking (momentum / pre-earnings / dealer hedging / informed / MNPI).

Options-spike signal triage

Industrial-electrification name with anomalous options positioning. Pre-earnings vs informed-flow framework applied.

Options-spike signal triage

GE Vernova call premium spike against the power-generation backdrop. Hypothesis discrimination by signal magnitude.

Options-spike signal triage

Halliburton unusual options activity ahead of energy-services cycle commentary. Flow-quality scoring layered on top.

Options-spike signal triage

Iron Mountain — REIT with elevated put/call skew. Distinguishing routine pre-earnings hedging from directional positioning.

Options-spike signal triage

MGM Resorts — anomalous near-dated options interest. Consumer-discretionary positioning frame.

Options-spike signal triage

Northern Trust — financials-name with elevated call flow against the rate-sensitivity context.

Options-spike signal triage

Super Micro — extreme call skew against the AI-server narrative. Informed-flow vs momentum-chasing discrimination.

Options-spike signal triage

Tractor Supply — call premium concentration in a rural-retail name. Hypothesis: pre-earnings drift or sector rotation read.

Options-spike signal triage

Warner Bros. Discovery — media-name elevated activity. Per-entity baseline calibration applied to filter ambient market state.

Options-spike signal triage

Accenture — services-name with concentrated call premium ahead of consulting-sector commentary. First in the options-spike series.

Options-spike signal triage

Costco — defensive consumer-staples name with anomalous options interest. Routine pre-earnings vs informed-flow framing.

Options-spike signal triage

Danaher — life-sciences exposure with elevated near-dated options activity. Distinguishing macro-rotation drivers from name-specific signal.

Options-spike signal triage

Dow Inc. — chemicals with put/call skew. Cyclical-pricing read layered on top of options-flow signal.

Options-spike signal triage

Live Nation — entertainment with anomalous call interest. Tour-season seasonality vs informed-flow hypothesis.

Options-spike signal triage

Walmart — defensive consumer-discretionary with elevated options interest. Consumer-spending read against the macro backdrop.

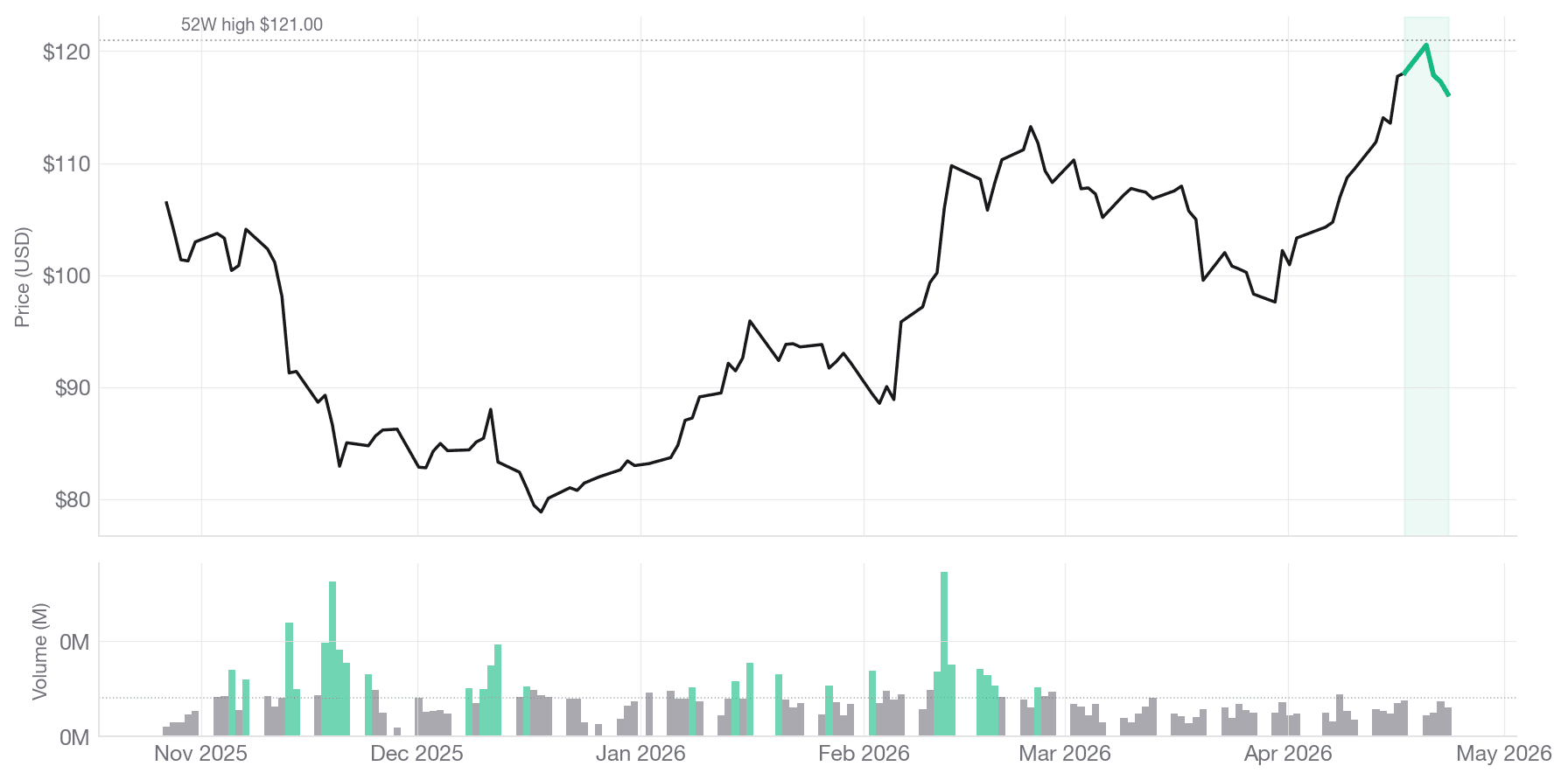

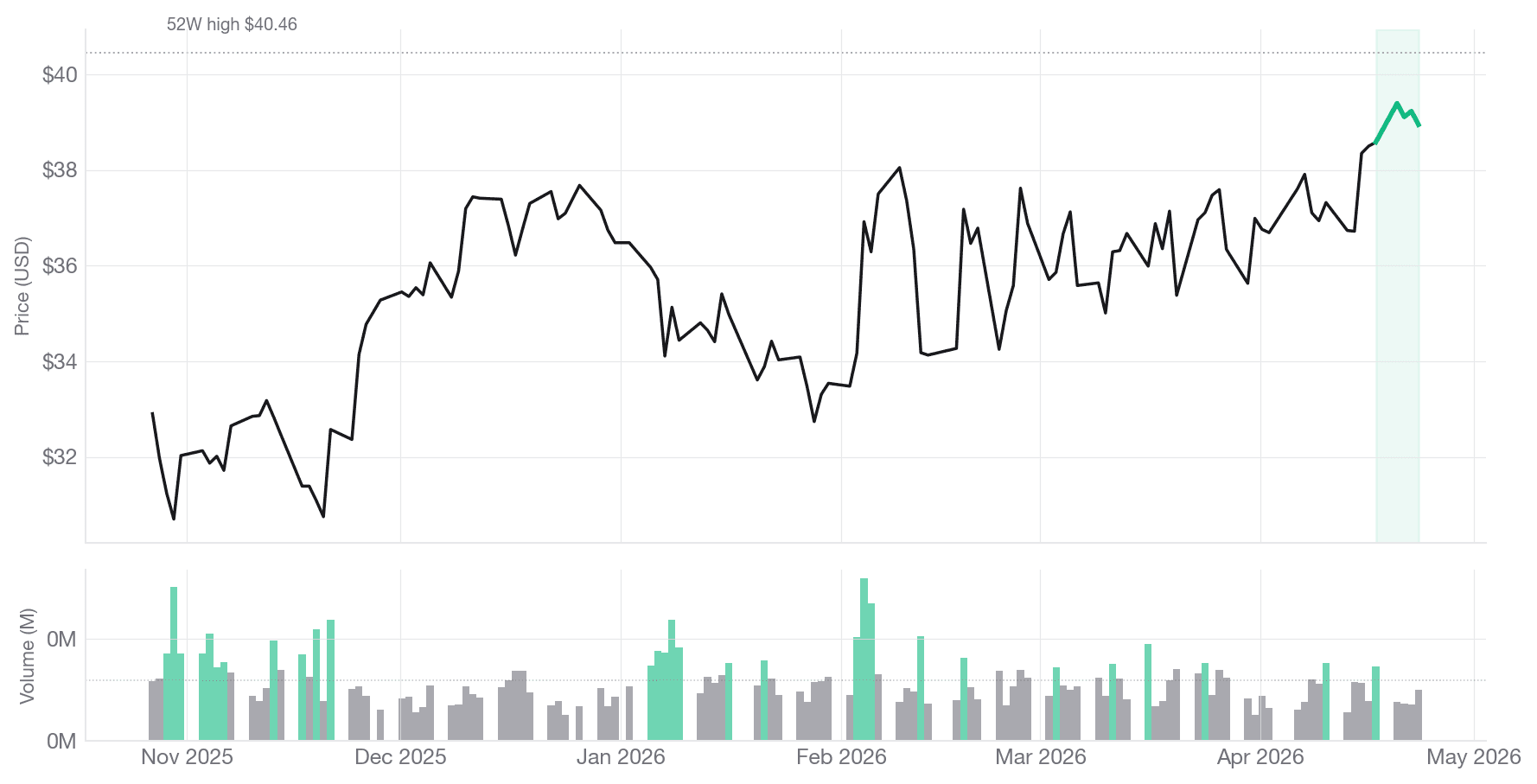

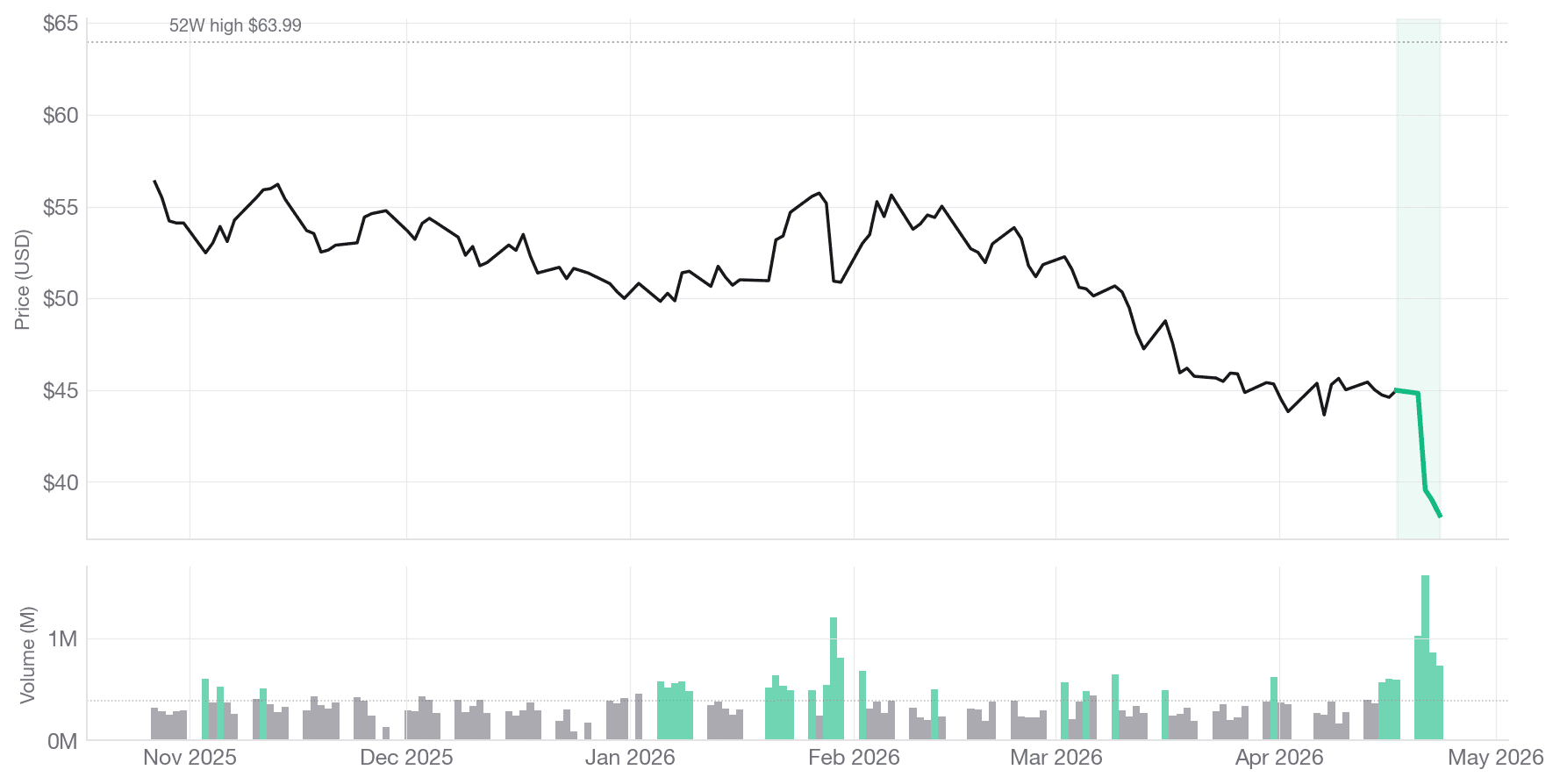

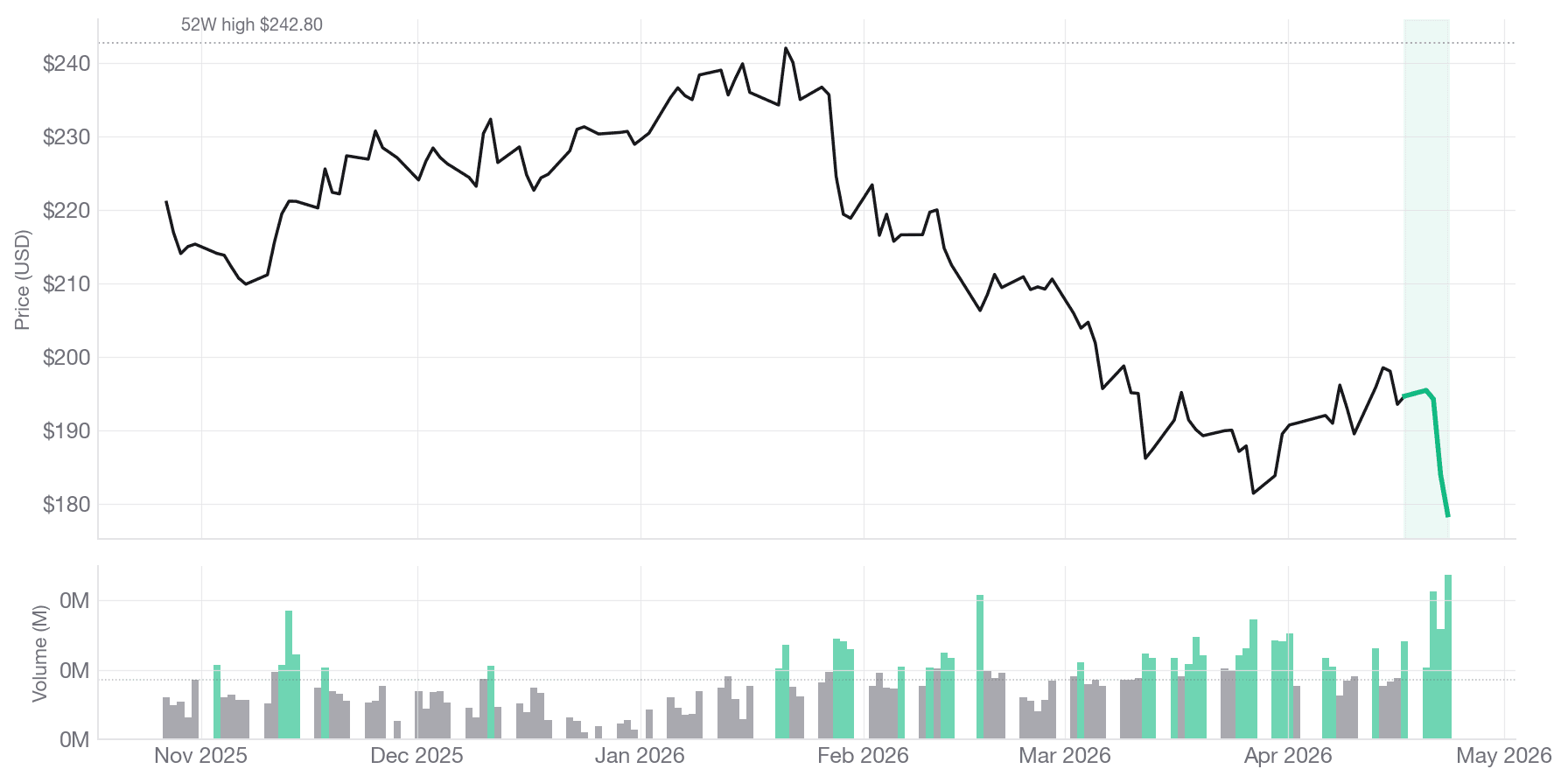

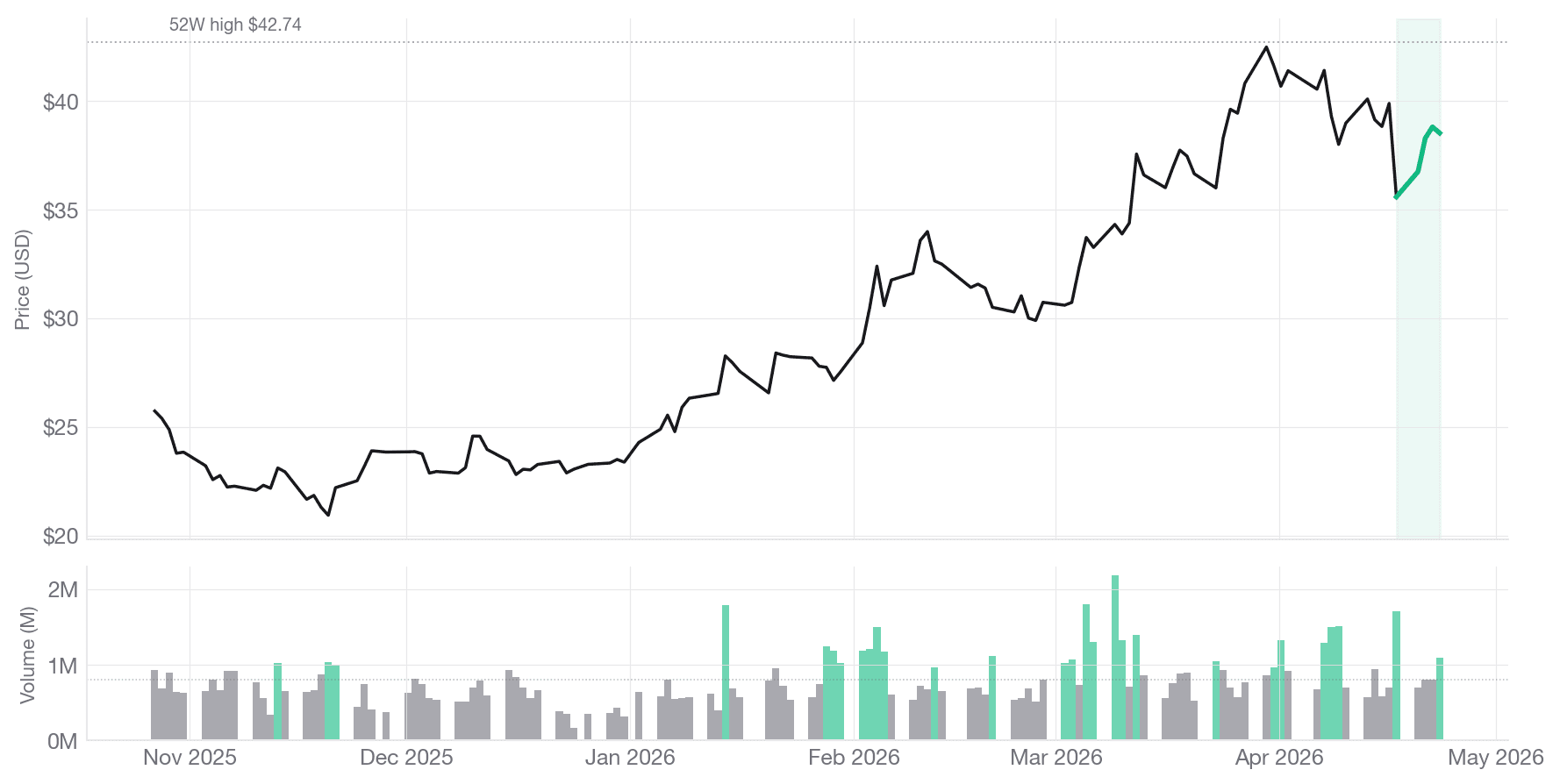

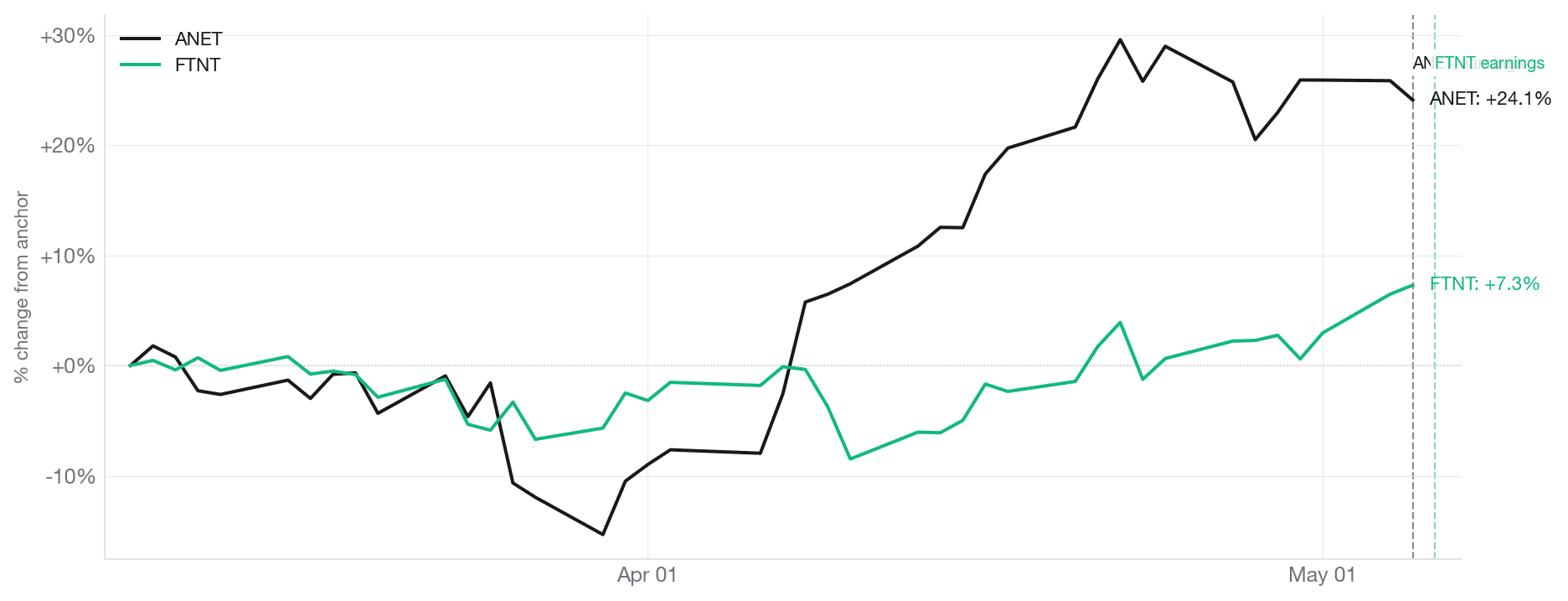

Q1 inversion — networking vs security

Comparative analysis. Arista Networks (networking) and Fortinet (security) printed inverted Q1 reactions despite shared AI-infrastructure-adjacent narratives. Cross-name signal-mix decomposition.

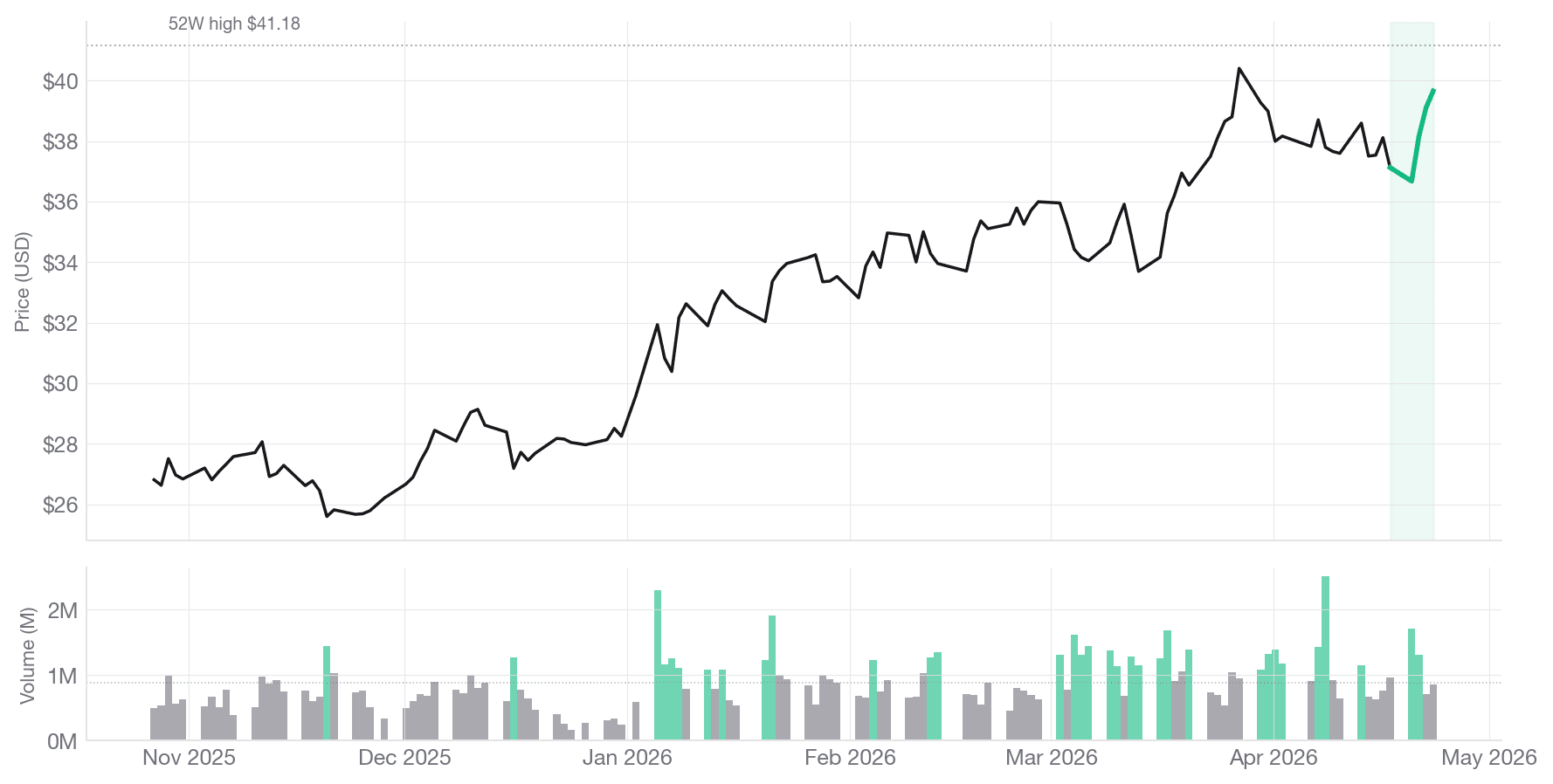

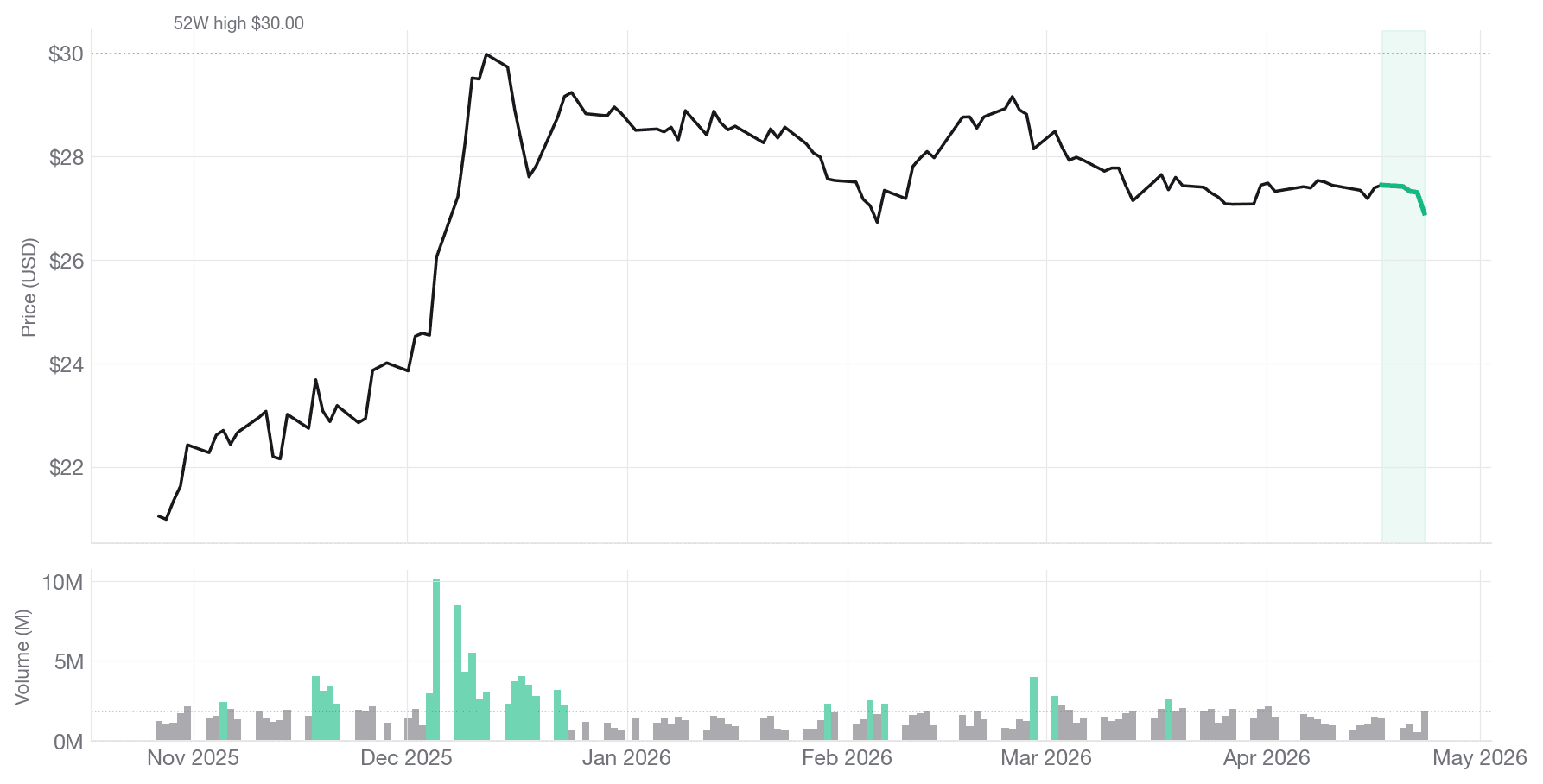

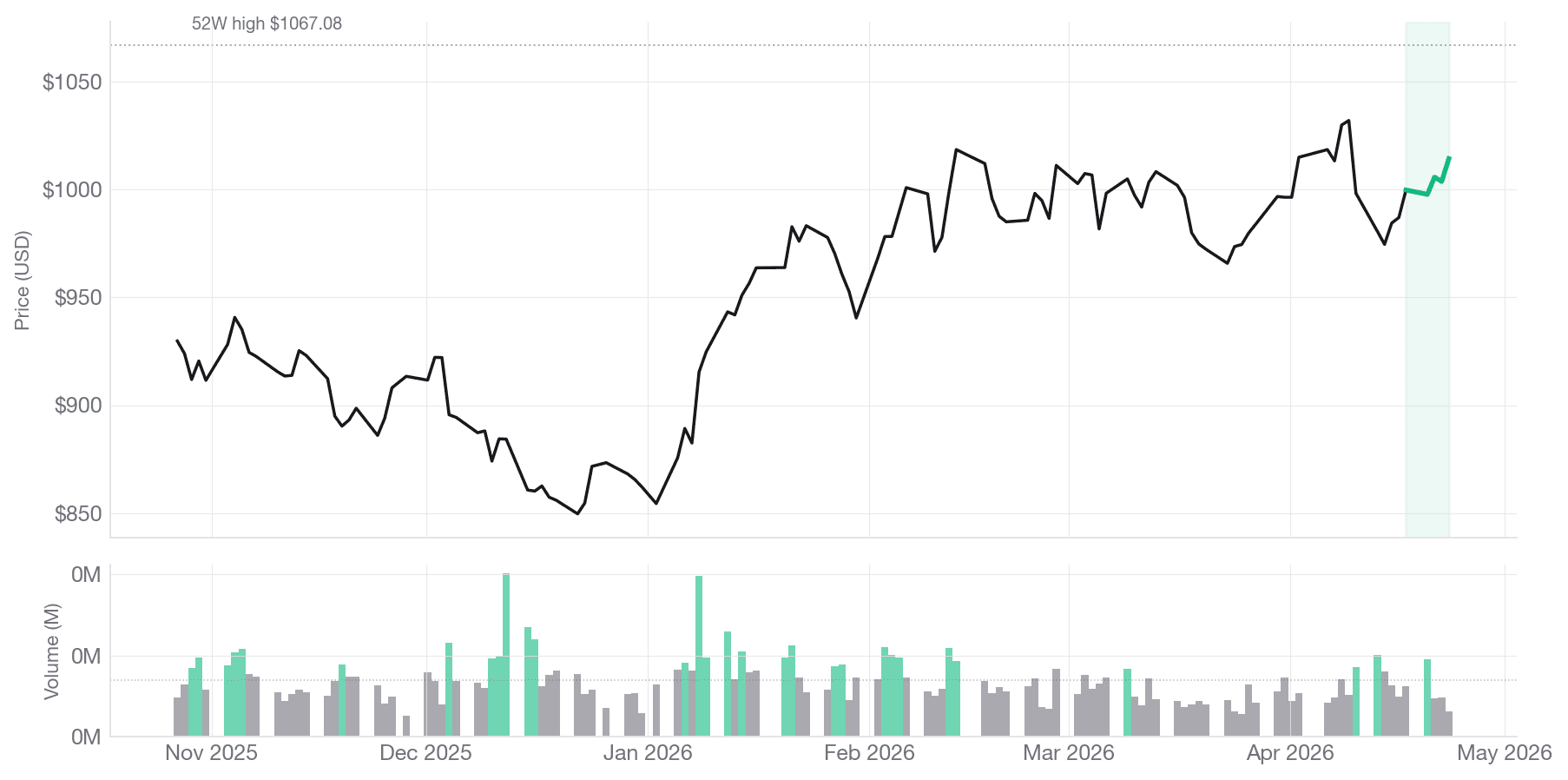

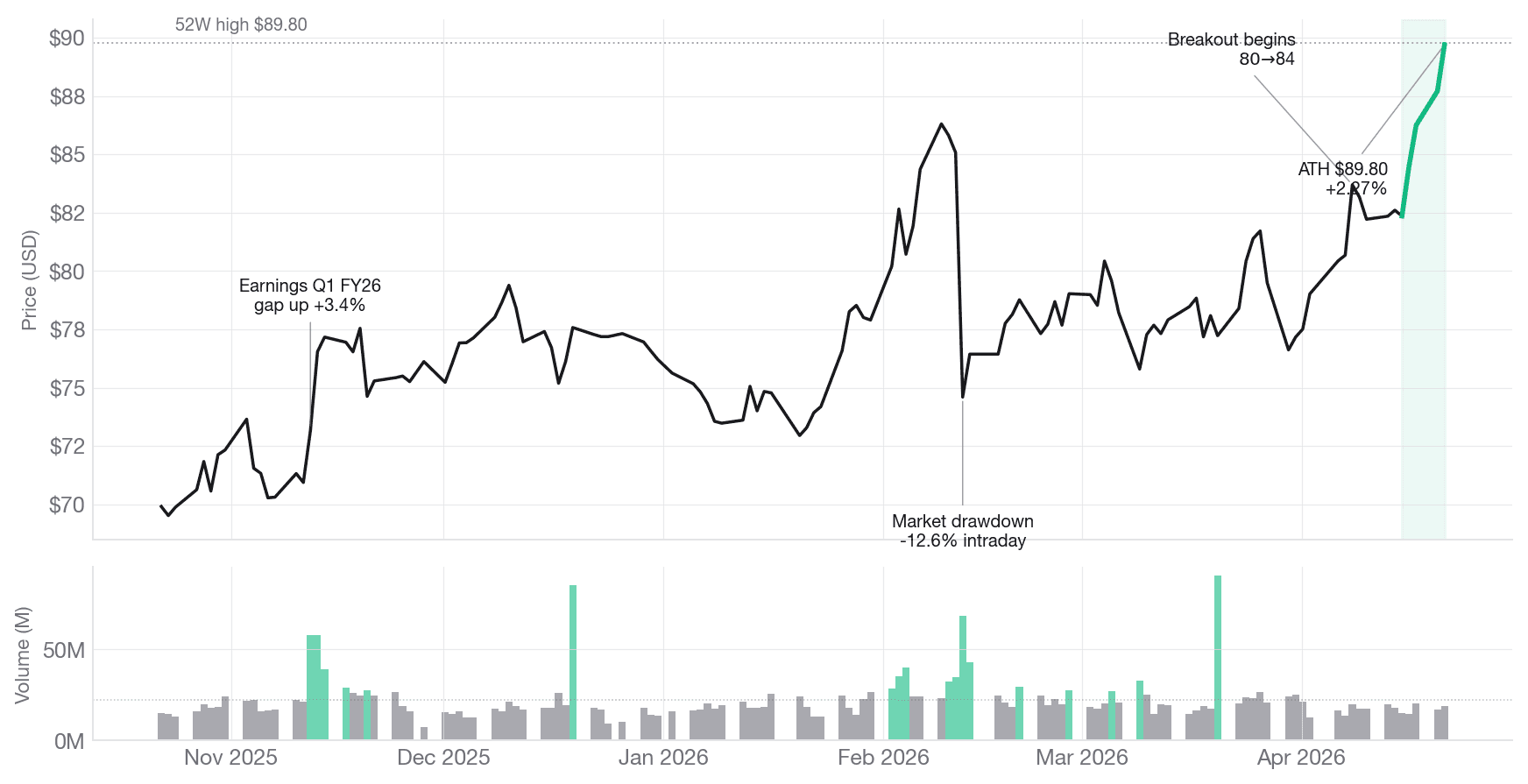

Breakout to 52W high

Pre-earnings technical breakout on rising volume. Combined signal-cache read (congressional + insider + institutional) framed the run-up. Proof-of-concept for the Unfair-branded research-note workflow.

Methodology

Notes are produced from a three-layer pipeline. Inputs are independent; synthesis is constrained. The same infrastructure runs every note.

Data layer

8 sources

Unusual Whales (options flow, dark pool, congressional, short interest, 13-F, ETF flows), Finnhub (analyst estimates, earnings), FRED (credit spreads, treasury, VIX), SEC EDGAR (Form 4, 8-K, XBRL), USAspending (government contracts), FINRA (short volume historicals), House Clerk + Senate EFD (PTR PDFs).

Signal layer

14 active signals

Each signal extends a common BaseSignal interface and outputs (direction, conviction, decay_rate). Combiner enforces macro-direction caps, per-signal contribution limits, correlation penalties, and a 0.15 dead-zone floor. Weights are SLSQP-optimized with L2 regularization and t-stat gating against a walk-forward 252-day in-sample window.

Research layer

PDF publication

Notes are matplotlib-charted, HTML-templated, Chrome-headless-rendered. Earnings call audio is captured live via yt-dlp and transcribed via Whisper-medium chunked. Transcripts feed an 8-pass analyzer (structure / Q&A directness / sentiment / forward-looking / numerical / hedging / mentions / FinGPT) before any narrative is written.

Backtest framing

Run 15-synced baseline: 14-year walk-forward, 8-signal long-only portfolio, half-Kelly sizing, 252-day in-sample / 21-day out-of-sample windows. OOS Sharpe 0.93, IS Sharpe 2.41, annual return 16.3%, max drawdown 28.9%, alpha 2.77. Conviction-threshold lock at 0.30. Survivorship-bias-free universe via historical S&P 500 constituent membership. Combiner guards documented; deactivated signals (volatility_regime, macro_regime) excluded from weight allocation. Live system runs the same combiner math as the backtester.

About

Unfair is a single-author quantitative equity research publication. Notes are published as PDFs and indexed here. All notes are free; there are no paywalls or tiered access.

The platform behind the notes is a 521-ticker signal pipeline with 14 active alpha generators, a constrained adaptive-weights combiner, and a Half-Kelly sizing framework with hard risk limits. The publication exists to make the analysis public and citable; the trading infrastructure remains private.

Notes are opinionated and cited. Every numerical claim traces to a primary source. Every signal reading reflects the platform's state at the timestamp noted. Past performance is not indicative of future results, and nothing published here is investment advice.

New research, in your inbox

Subscribe

Get an email when a new research note is published. Notes ship when there's something worth publishing — no fixed cadence, no marketing sequences, no promotional content. Double-opt-in. One-click unsubscribe.

We use Resend for delivery. Email is stored only to send research notes and is never shared. See Privacy.